We handle permits, inspections, utility coordination, demolition, and cleanup — so you don’t have to stress or guess

Will Homeowners Insurance Cover Mobile Home Demolition After Storm Damage?

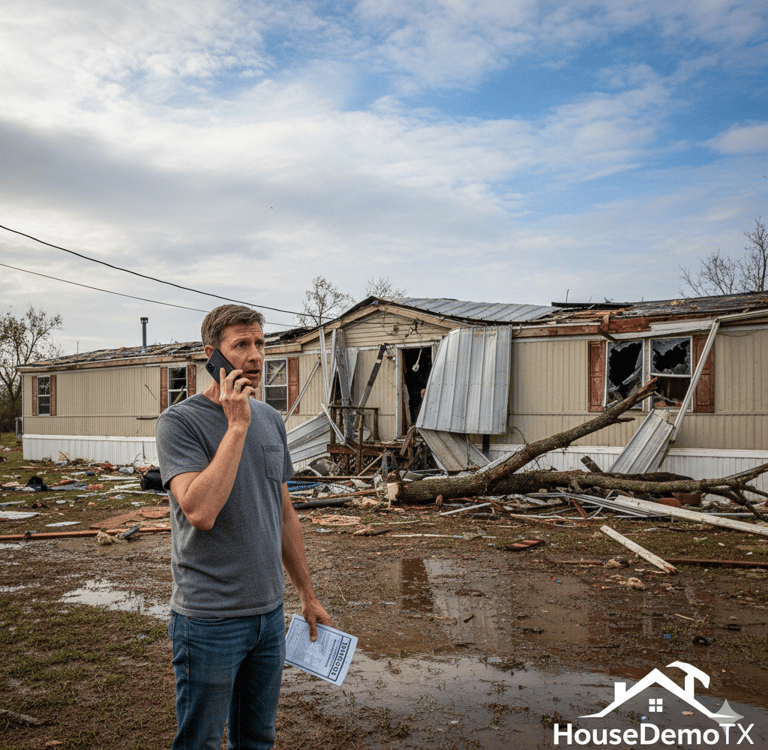

After a severe Texas storm—whether it's a hurricane along the coast, a tornado in North Texas, or a widespread freeze—many mobile homes are damaged beyond repair. The question then arises: Will your homeowners insurance policy cover the demolition costs? In 2026, the answer is nuanced, depending heavily on your specific policy, the cause of damage, and whether the mobile home was considered "real property." At HouseDemoTX, we work with homeowners and insurance adjusters to provide clear, itemized demolition quotes that meet industry standards. Here’s a breakdown of what you need to know.

MOBILE HOME DEMOLITION

1/30/20262 min read

Will Homeowners Insurance Cover Mobile Home Demolition After Storm Damage?

1. Dwelling vs. Other Structures Coverage (And the "Real Property" Clause)

Most standard homeowners insurance (HO-3 or HO-A in Texas) covers the dwelling (your primary home) and other structures (like sheds or detached garages). The key factor for a mobile home is how it’s classified:

"Real Property" (Usually Covered): If your mobile home is permanently affixed to a foundation (e.g., concrete slab or runners) and has been "converted" from personal property to real property (meaning it has a new tax ID and is no longer titled as a vehicle), then its demolition after a covered peril is typically included under Dwelling Coverage.

"Personal Property" (Limited Coverage): If your mobile home is still on wheels, piers, or is considered "personal property" (i.e., you still have a vehicle title for it), its coverage is more complex. It might fall under Other Structures (which usually has a lower coverage limit, often 10% of your dwelling coverage) or even Personal Property coverage, which usually doesn't include demolition.

2. Covered Perils vs. Exclusions

Your policy will only cover demolition if the damage was caused by a covered peril.

Common Covered Perils (Usually Include Demolition):

Fire

Windstorm/Hail (e.g., hurricane, tornado)

Lightning

Vandalism

Weight of ice, snow, or sleet

Common Exclusions (Demolition Not Covered):

Flood: Standard homeowners insurance never covers flood damage. You need a separate National Flood Insurance Program (NFIP) policy. If the home is totaled by a flood, that policy might cover demolition and debris removal, but it's not guaranteed.

Earth Movement: Earthquakes or sinkholes are typically excluded unless specifically added by endorsement.

Neglect/Wear and Tear: If the home simply deteriorated over time, demolition won't be covered.

3. Debris Removal Limits

Even if the damage is from a covered peril, your policy will have limits for debris removal.

Typical Limits: Most policies offer 5-10% of the dwelling coverage amount for debris removal, in addition to the dwelling limit itself. For example, if your dwelling is insured for $100,000, you might have an extra $5,000-$10,000 for debris removal and demolition.

"Reasonable Costs": Insurance companies will only pay for "reasonable" demolition and debris removal costs. This is where HouseDemoTX's itemized quotes help, showing fair market value for labor, equipment, and disposal.

4. The Adjuster's Role & "Total Loss"

Total Loss: Your insurance company will send an adjuster to determine if the mobile home is a "total loss" (meaning the cost to repair exceeds a certain percentage of its value). If it is, they will usually approve demolition.

ACV vs. RCV: Be aware if your policy pays out on Actual Cash Value (ACV) or Replacement Cost Value (RCV). ACV deducts for depreciation, which can significantly reduce the payout for an older mobile home, potentially leaving you with less to cover demolition.

Insurance Demolition Checklist

Action Why It Matters

Review Your Policy Confirm "real property" status & debris removal limits.

Document Damage Photos/videos before any cleanup.

Get Itemized Quote HouseDemoTX provides detailed estimates for adjusters.

Communicate with Adjuster Keep them informed of all steps and costs.

HouseDemoTX Insight: For older, heavily damaged mobile homes, sometimes the cost of demolition can exceed the "Other Structures" coverage. In such cases, negotiating with your adjuster for a higher payout, especially if the structure poses an immediate hazard, is crucial.

Navigating the Aftermath of a Storm

Dealing with storm damage is stressful enough. Let HouseDemoTX handle the demolition with professional, insurance-ready services. We help streamline the process from quote to clear lot.